Seed-Stage Dealflow is declining in America as AI Funding reshapes Venture Capital, squeezes the Startup Ecosystem, dries Early-Stage Investment, and leaves many US Startups struggling to raise meaningful rounds.

The startup ecosystem that once celebrated variety is now dominated by capital chasing machine learning and automation. As a result, thousands of US startups in non-AI sectors face a funding drought that threatens innovation.

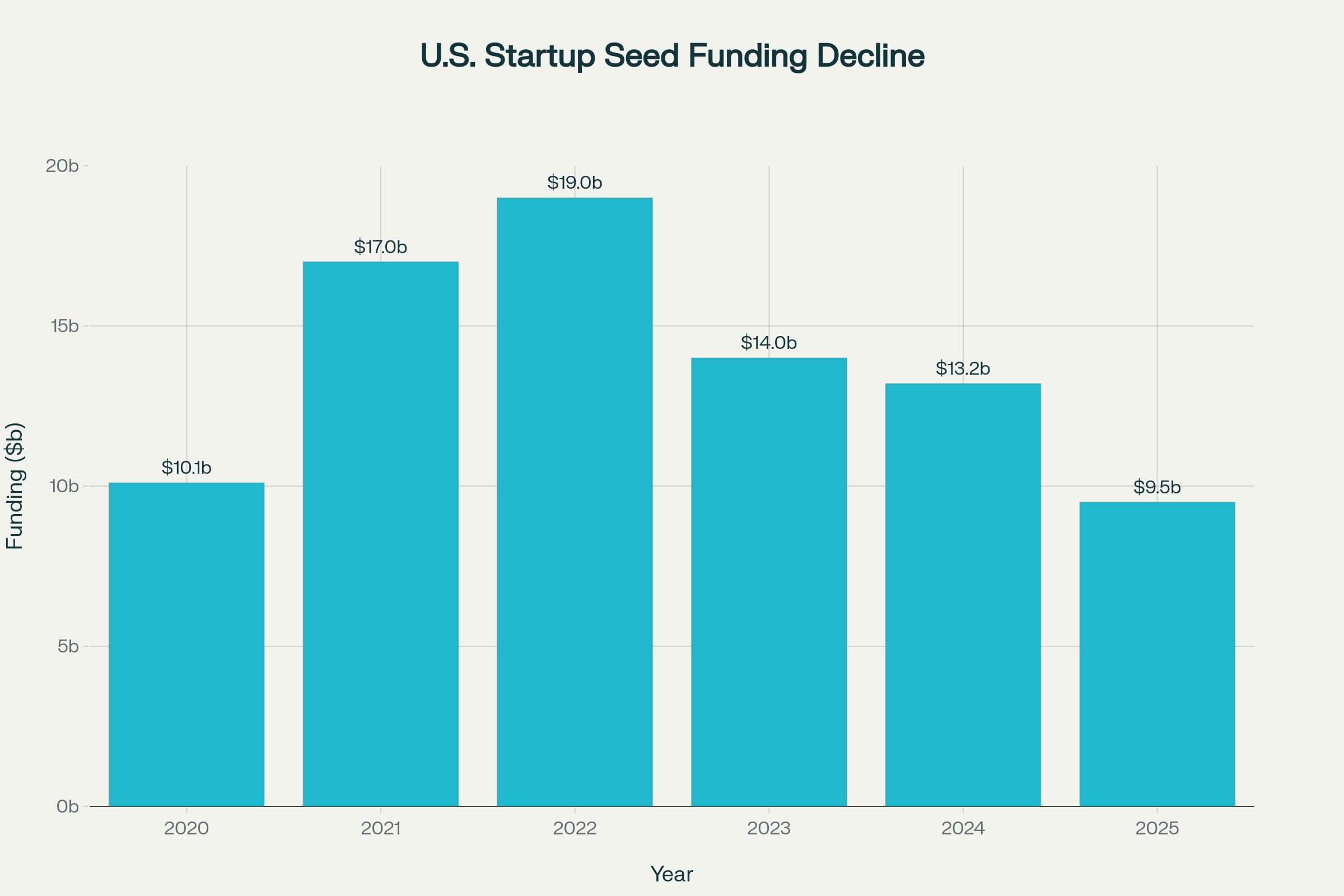

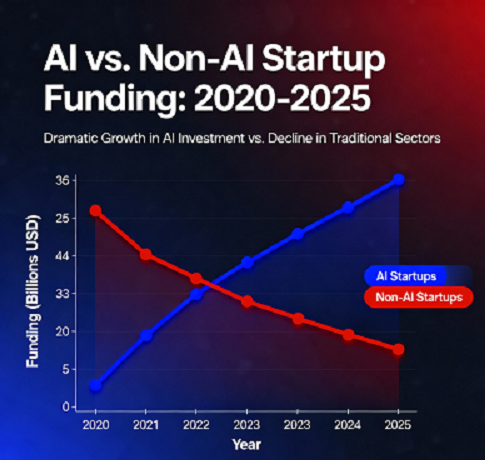

The numbers tell the story. Seed funding across the US dropped to around $4.6 billion in Q3 2025, less than half its pandemic-era highs. At the same time, AI funding accounted for more than 60 percent of all North American startup capital.

In 2024 alone, four states captured over 72 percent of total US venture capital activity, with California’s share nearing 49 percent. The outcome is a lopsided startup ecosystem, where fewer companies raise much larger rounds while the rest are left behind.

This trend signals a structural shift rather than a temporary correction. When money flows overwhelmingly to one technology, early-stage investment diversity weakens, and the country’s creative pipeline narrows.

The Rise of AI and the Shrinking Base

The explosion of AI funding has changed how investors view risk and opportunity. Between 2023 and 2025, mega-rounds in AI companies, from model developers to chip designers, absorbed nearly all new venture capital inflows. Startups such as OpenAI, Anthropic, and Scale AI attracted billions, while smaller founders struggled to close $2 million rounds.

Historically, seed-stage dealflow provided the foundation for America’s entrepreneurial cycle. It funded early experiments, from e-commerce to clean energy to social apps. Even promising founders outside AI must redesign their pitch decks to include “AI-driven” or “AI-assisted” solutions to get meetings.

Meanwhile, industries that once drew steady early-stage investment —such as foodtech, ag-tech, and healthtech —are collapsing under investor indifference. Food & beverage startups saw funding fall by 47 percent in 2024.

Cannabis seed rounds hit decade lows. Even AR/VR ventures, once touted as “the next frontier,” dropped by two-thirds. US startups in these sectors are cutting teams, extending runways, or pivoting entirely to survive.

The Geography of Decline

The collapse in seed-stage dealflow also has a geographic face. States that anchored the first wave of tech entrepreneurship are pulling even further ahead. California, New York, and Washington remain strong, buoyed by AI clusters and top research institutions. But Massachusetts, long a biotech stronghold, saw its venture capital share shrink from nearly 13 percent in 2023 to just 8 percent in 2024.

The South and Midwest fared worse. Texas, Florida, and Illinois each lost ground, while many smaller hubs like Cleveland, Nashville, and Denver reported negligible new rounds. These regions built emerging ecosystems over the last decade, but their startup ecosystem looks increasingly hollow. The concentration of AI funding reinforces this divide, with coastal cities drawing talent and dollars while the heartland loses early momentum.

For policymakers, this uneven early-stage investment pattern raises long-term competitiveness concerns. If local entrepreneurs cannot access funding, regional economies risk stagnation, and innovation migrates to already dominant hubs. The health of US startups nationwide depends on correcting this imbalance.

The Changing Role of Angels and Accelerators

Even as traditional venture capital firms pull back, other investors are adapting. Accelerators like Y Combinator still enroll large cohorts—249 in Winter 2024—but the nature of their follow-on rounds has shifted. Many founders now close smaller rounds through angel investors, often $1.5 million or less. These angels fill gaps left by institutional funds but cannot scale the entire market.

The dynamics of seed-stage dealflow have also changed at the negotiation table. Venture funds once sought 10 percent ownership in seed rounds; now, founders prefer smaller checks at lower dilution, accepting that valuations and speed matter more than size. The shift has compressed deal terms but expanded uncertainty for the next round of funding.

Corporate venture teams and innovation labs show a similar pattern. Big players like Amazon and Google are channeling AI funding toward mature startups or internal R&D. Few corporate programs now invest in very young companies, especially outside AI. As a result, early-stage investment is increasingly detached from long-term corporate acquisition strategies—a gap that could stifle collaboration and exit opportunities for US startups.

The Sectoral Fallout

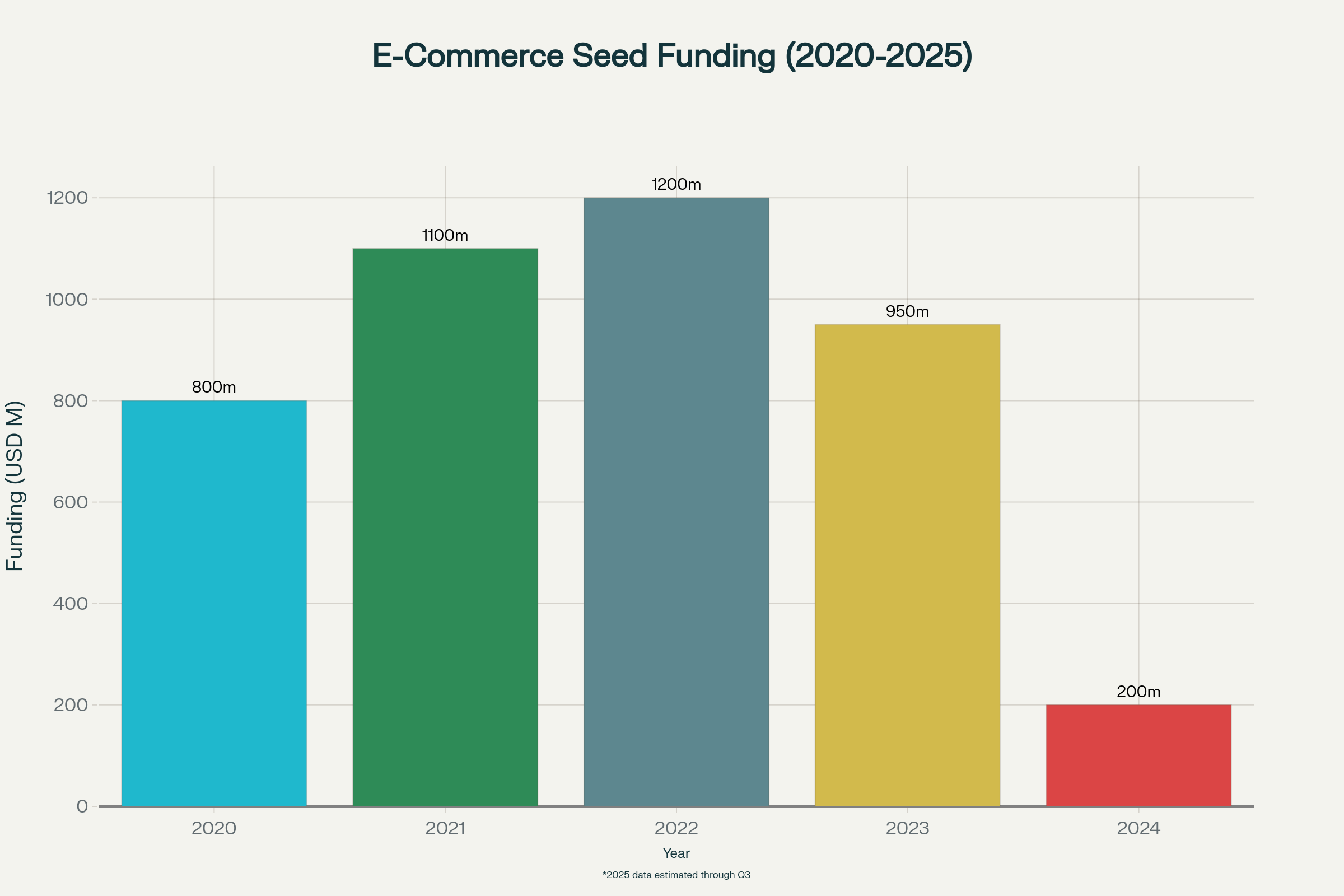

The funding imbalance is evident in sector data. Foodtech and alternative proteins lost momentum after weak exits. Consumer apps and e-commerce startups, once magnets for venture capital, are now struggling to attract seed checks. In 2024, e-commerce seed funding plunged from over $1 billion pre-2023 to just $200 million.

On the other hand, AI-adjacent verticals like automation, AI infrastructure, and cybersecurity are booming. The startup ecosystem has effectively split into two worlds: those that can articulate an AI narrative and those that cannot. Biotech, fintech, and energy are seeing AI creep into every major deal. If this continues, seed-stage dealflow for non-AI founders may dry up completely.

This narrow focus creates fragility. The US has historically led innovation because of its variety, not uniformity. If only AI-driven ideas attract early-stage investment, the country risks missing out on materials science, space tech, or sustainable manufacturing breakthroughs.

Why the Pipeline Matters

Seed rounds fund experimentation, the unglamorous but vital phase of innovation. The entire startup ecosystem loses resilience when AI funding dominates to this degree. The fall in venture capital diversity translates into fewer experiments, fewer job creators, and fewer moonshots.

The NVCA and PitchBook report that US seed deals dropped from over 1,700 per quarter in early 2022 to fewer than 800 by mid-2025. Such contraction means the early-stage investment pipeline that once powered Silicon Valley’s dynamism now runs thin. The country’s R&D engine is sputtering because many promising US startups have never made it past concept.

To reverse this, investors and policymakers must rethink capital allocation. Tax incentives, regional fund-of-funds, and AI-balanced portfolios could revive seed-stage dealflow without undermining the gains from the AI surge. Innovation depends on variety; AI may lead the present, but diversity secures the future.

The United States stands at a crossroads. Seed-stage dealflow is shrinking, yet AI funding keeps breaking records. Venture capital must balance efficiency with breadth, ensuring the startup ecosystem stays open to novel ideas. Strengthening early-stage investment across all regions can restore equilibrium and unlock the next generation of US startups beyond the AI boom.

Follow USTechTimes on Facebook, Twitter and Linkedin for in-depth news of market trends, funding updates, and regulatory changes affecting startups in USA.

We Recommend:

- Rockset Raises $44 Million to Expand Real-Time Analytics Database Capabilities

- Energize Capital Closes $300M Growth Fund, Surpasses $1.2B Assets Under Management

- Denver-Based BillingPlatform Secures $90 Million Investment for Global Expansion

- Linxup Secures $50M Boost from Runway Growth Capital for GPS Tracking and Fleet Management Excellence

- Mediafly Announces $80 Million Funding Round to Accelerate Enterprise Revenue Enablement

{kind=link}